There are many factors to consider when determining whether refinancing a mortgage is worth it, such as interest rate fluctuations, your home value, your credit score and when you are planning to move. In many circumstances, refinancing can save money on total interest over the life of your loan or on your monthly mortgage payment.

You should carefully consider whether it’s the best time to refinance your home loan before you apply. This means determining whether refinancing makes financial sense. A loan expert at Homesite Mortgage can help you calculate your potential savings against the costs associated with refinancing your loan.

Can I Save by Refinancing?

Refinancing your mortgage means paying off your existing home loan and taking on a new one. There are a few ways in which refinancing your home loan can save you money.

- Utilize equity: If you have equity, you can refinance and utilize this equity to cover major expenses or pay off other debt. Taking on a low-interest mortgage to pay off high-interest debt can save you money in the long term. You can also use the extra cash to invest in home improvements or higher education that could lead to more income or greater returns down the road.

- Eliminate PMI: In some cases, you may be paying private mortgage insurance (PMI) on top of your principal and interest. Eliminating PMI can save you thousands each year.

- Lower the interest rate: One of the best ways you can save money with a refinance is by securing a lower interest rate on your existing home loan. Not only can you save money by lowering your interest rate, and thus, the amount of interest you pay on the loan, but you can also speed up the process of building equity and decrease your monthly payment, as your interest per month will be lower.

- Lower the monthly mortgage payments: If refinancing can lower your monthly payment, you can save money month to month. Even a few hundred dollars can add some much-needed wiggle room to your budget, or you can allocate this savings to another financial goal.

- Shorten the duration of the loan: Finally, you can save by shortening your loan’s term. With a shorter term, you can significantly reduce the total interest you pay on your loan.

Scenarios in Which Refinancing Could be Beneficial

Refinancing can be beneficial when it makes financial sense for you. However, whether something makes financial sense not only depends on your budget and income but on your goals as well. Is your goal to save in total interest you must pay on the home loan, to lower your monthly payment or to use cash from your home’s equity? Refinancing could be beneficial in the following scenarios.

1. Your Credit Score Has Increased

Lenders consider credit a crucial factor when calculating a mortgage interest rate. Typically, the better your credit score, the lower your interest rate will be. While you may be able to obtain a mortgage with a credit score of 620, your interest rate will be significantly different from someone with a credit score of 740.

For example, a borrower with a credit score of at least 740 and a 20% down payment typically receives a 30-year fixed rate approximately 0.5% lower than a borrower with a 680 credit score and a 20% down payment. You may also want a higher credit score depending on other factors, such as whether you have a smaller down payment. Fortunately, even if you have less-than-stellar credit, you can take the following steps to improve your credit:

- Eliminate old debt

- Monitor your score

- Make every payment on time

- Reduce your credit card balances

- Address delinquency periods by calling a credit agency

Download our free credit score improvement checklist to give your credit score the boost it needs.

2. You’ve Noticed Interest Rates Have Dropped Compared to Your Current Interest Rate

Interest rates for mortgages fluctuate depending on a variety of factors, such as the economy, inflation, global factors, market movements and the monetary policy set by the U.S. Federal Reserve. If mortgage interest rates drop and you can get a lower interest rate, you could spend less on interest over the duration of your home loan.

However, the rule of thumb for refinancing is that you should only consider a refinance if you can lower your interest rate by at least 2%. If you can only lower your interest rate by 0.5%, for example, the closing costs and hassle may not be worthwhile.

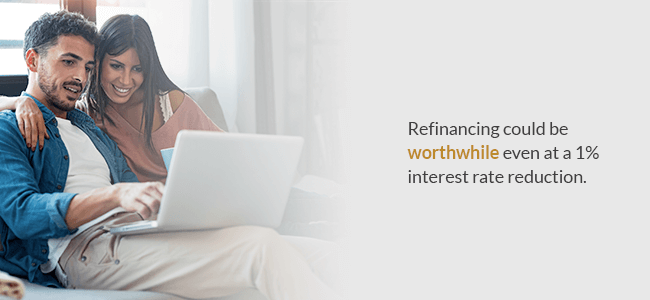

Of course, this rule of thumb varies depending on how long you plan on staying in the home. If you plan to live in your home longer than five years, for example, refinancing could be worthwhile even at a 1% interest rate reduction. Since refinancing affects your loan term, you should do the calculations to make sure refinancing still makes financial sense. If you need assistance, a loan expert at Homesite Mortgage can help.

3. You’ve Had a Change in Relationship Status

If you co-own your home with an ex-spouse, you may want to refinance your mortgage to get your ex off the loan. During a divorce, the spouse who will keep the home typically must refinance to get the other owner off the existing loan. This also applies when the co-owner is a business partner, friend, relative or significant other. To buy out your ex-spouse, refinancing your home loan may be the best route, especially if you can do so before rates rise.

If you’ve recently gotten married and already own a home, you may also want to refinance to add your new spouse to the mortgage, especially if your spouse has additional income and good credit.

4. Your Home Value Increased

When the value of your property rises, it may be beneficial to refinance your home loan, especially if you have another major financial goal or other high-interest debt you want to pay off. An increase in your home value can mean you’ve gained equity, which you can leverage to improve your financial situation.

For example, if you opt for a cash-out refinance, you will take out a new home loan that is larger than what you owe on your original mortgage and receive the difference between your original mortgage and new mortgage in cash. Maybe you want to use this cash to make home improvements or to cover your child’s college tuition. If you go this route, you should ensure you won’t pay more in mortgage interest than you will in interest for the debt you’re using the cash to eliminate.

5. You Want to Shorten the Loan Duration

Refinancing to a shorter loan term can help you pay off your debt more quickly. If you manage to lower your interest rate and reduce your loan term, you could potentially save a significant amount of money over the duration of the loan. When you shorten your loan term, you pay less in total interest.

Keep in mind, though, that a shorter loan term usually means a higher monthly mortgage payment. To ensure refinancing to a shorter loan term makes financial sense, be sure this new monthly payment will comfortably fit into your budget.

6. You Want to Lower Your Monthly Payments

If your monthly mortgage payment has been stretching your budget thin, you may want to refinance to get a lower payment. With a lower monthly mortgage payment, you’ll have more wiggle room in your budget, and you can maximize your monthly savings to meet your unique financial goals. You can save for an emergency, pay off high-interest debt or fund renovations that could increase your home’s value.

Alternatively, you may even want to refinance if you can afford a higher monthly payment. When you shorten your loan term, your monthly payment may increase, but by paying your loan off faster, you could save significantly in the long term.

7. You Plan to Live in Your Home for a Couple of Years After Refinancing

As long as you’re planning to live in your home for at least a couple of years, refinancing could make financial sense. If you want to move soon and already have a new home in mind, however, refinancing may actually lead to a loss. Before refinancing, calculate your breakeven point to ensure you won’t be losing money when you factor in refinancing costs.

Even if Your Loan is Newer, Refinancing Could Still Save You Money

We’ve seen people with loans from 2020 and 2021 still benefit from refinancing. There is no limit on how many times you can refinance your mortgage, so refinancing may still be worthwhile in your case.

While it’s not generally advisable to refinance multiple times within a short duration, we are in a unique time with low interest rates, so even those who purchased a home recently could still benefit from refinancing with a lower interest rate. Sometimes, this is actually more ideal because the longer you live in your home and pay toward your mortgage, the longer you see the benefits of refinancing.

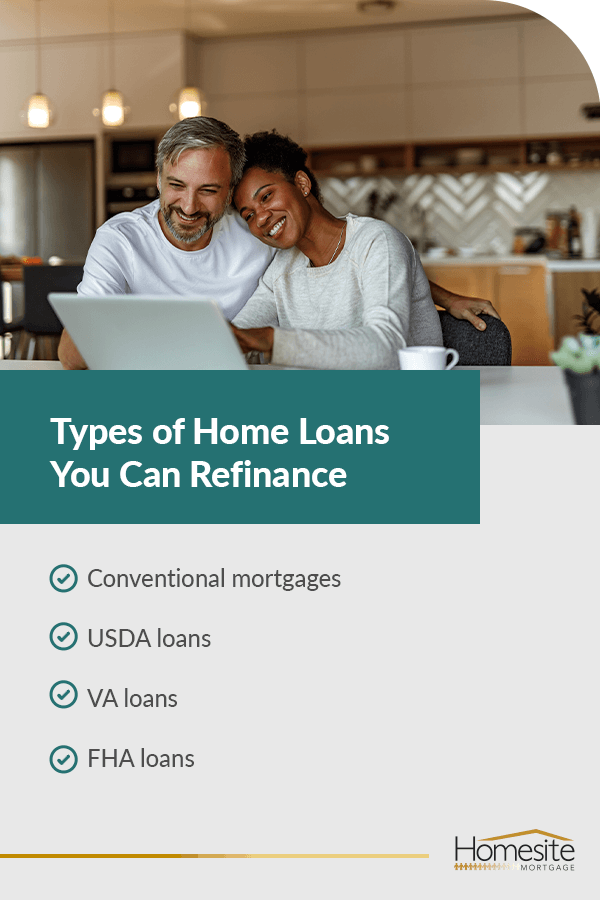

Types of Home Loans You Can Refinance

There are a few types of home loans you can refinance, including conventional mortgages, USDA loans, VA loans and FHA loans.

- Conventional mortgages: The most common home loan type, the conventional mortgage, can be refinanced. This type of loan is not backed by the federal government, though conventional loans must adhere to guidelines set by Fannie Mae and Freddie Mac.

- USDA loans: USDA loans may also be able to be refinanced. These loans are great for borrowers who don’t have a down payment and live in an eligible rural or suburban area.

- VA loans: Veterans can apply for a VA loan, which is backed by the U.S. Department of Veteran Affairs. This type of loan allows for 100% cash-out refinancing that you can use as you see fit, such as to make home improvements or pay off debt.

- FHA loans: FHA loans are great for borrowers who are struggling to save for a down payment. With an FHA loan, you can secure a home loan with just 3.5% down. If you have an FHA loan, you may be able to refinance as much as 97.75% of your home’s value.

Typical Costs Associated with Refinancing a Home Mortgage

Similar to when you closed on your original home loan, you may need to pay closing costs when you refinance. These costs may include an appraisal, title insurance, taxes, transfer fees and attorney’s fees. The simplest way to determine the potential costs for refinancing your mortgage is by reviewing your initial mortgage agreement. This will list lender and non-lender fees.

(This will have special attention brought to it when implemented on page) Keep in mind that the cost associated with refinancing is considered an investment. Therefore, the time it takes to recoup the investment is considered the return on investment period. We offer a zero-cost refinance loan so your return on investment is immediate.

Some Lenders May Provide Grants to Help Cover Those Costs

Grants help to lower the added cost of refinancing. Grants can absorb some, or all, of the closing costs associated with a refinance, which means a zero-cost refinance for you. Homesite Mortgage provides a grant so that your refinance can truly be at no cost! Check out our FHA lender grant for a limited time only or contact a loan expert to see how much you can save by refinancing with us at Homesite Mortgage.

How to Determine if Mortgage Refinancing is Right for You

So is refinancing worth it for you? There are many factors that can influence a home loan. It’s recommended to reach out to a loan expert, who can consider your options and advise what loan scenario is best for your refinance. Below are ways you can get a rough idea of whether refinancing is right for you.

- Figure out the interest rate you’re expecting to lock in: Request an interest rate quote from us at Homesite Mortgage to learn more about the interest rate you can expect to lock in if you refinance.

- Utilize a refinance calculator: Our mortgage refinance calculator can help you determine how much you could save on the lifetime of your loan by refinancing.

- Get approved and lock in your rate: You don’t want to wait long as rates could always go up. So once you’re approved, lock in your rate and finance your mortgage.

Keep in mind that it’s always advisable to consult a loan expert to determine whether refinancing is right for you.

Is It Too Late to Refinance and Save Money?

Though it’s still a great time to refinance, the industry is buzzing that interest rates will be going up soon — so lock rates in now. At Homesite Mortgage, we are your source for flexible lending and great rates.

Our loan experts at Homesite Mortgage can help you meet your refinance goals. But don’t wait too long with the strong potential for rates to increase soon! Schedule an appointment with a mortgage expert at Homesite Mortgage today to determine whether refinancing is right for you.